Why the cloud investment opportunity will outlast an economic downturn

November 2022

The global shift to cloud computing is a seismic and transformational trend that we have backed for several years at Magellan.

For the hyperscale public cloud vendors outside China – Amazon, Microsoft, and Google (the MFG Global Fund holds all three companies) – it has created unprecedented market opportunity. These vendors have consistently generated strong double-digit revenue growth at scale and continue to do so to this day. Yet in the most recent two financial quarters, hyperscale cloud revenue has faced decelerating growth as enterprise customers reign in spend amid the uncertain macroeconomic backdrop. Has the story come to an end?

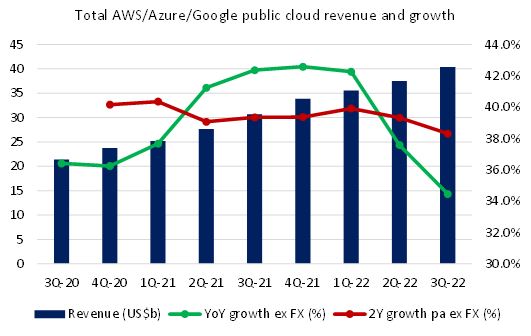

Note: Blue bars represent aggregate quarterly cloud revenue of Amazon Web Services, Microsoft Azure (MFG estimate), and Google Cloud. Green line represents the quarterly year-over-year growth rate. Red line represents the growth rate compared to two years ago on an annualised basis. Growth rates are in constant currency to reflect underlying growth.

The trend this year is apparent. Excluding the impact of currency movements, hyperscale cloud revenue grew in aggregate 42% year-over-year in Q1. In Q2, the growth rate fell to 38%, and in the most recent Q3, the growth fell further to 34%. The two largest vendors, Amazon and Microsoft, expect this deceleration to continue, which means we should expect the growth rate to decline even more in Q4. On top of that, margins are falling, with both companies dealing with rising energy costs in their data centres while continuing to maintain their pace of double-digit operating expense growth. All of this may seem dire but let us unpack it further.

We start by recognising that the deceleration this year appears more severe because it is being compared to several quarters of strong growth in 2021 due to cloud demand created by the pandemic responses. To try to adjust for this by looking at this year’s quarterly growth rates on a 2-year annualised basis, we see a steadier growth trend, albeit one that is still slowing – from 40% in Q1, to 39% in Q2, to 38% in Q3. (The fact that we are seeing this type of growth on an aggregate US$160 billion in annualised revenue is staggering on its own). These decreases are more marginal and subject to noise, but there is broader evidence that IT spend is generally tightening.

The unfavourability of these recent IT spending trends are, we believe, cyclical not structural. Market uncertainty has compelled enterprise customers to become more prudent or selective about their IT investments. Some customers are in industries facing challenges of their own such as supply chain issues, inflation, or labour shortages. We also expect some spend was driven by the period of excessive cheap, available money and this spend will not return. And as their customers seek to tighten their belts, hyperscale cloud vendors are taking it a step further and in fact helping customers to improve the efficiency of their spend (e.g., through lower priced options). In other words, the cloud vendors are effectively contributing to their own growth headwinds.

Why do this? It is about driving trusted partnerships with customers for long term growth, rather than short-sightedly focusing on maximising growth today. This makes sense if one believes, as we do, that cloud has a significant multi-year growth runway ahead. In fact, the ability for customers to proactively dial up and down cloud spend according to their needs – rather than being burdened with the large, fixed costs of an on-premises data centre when times are tough – is one of the fundamental value propositions of the cloud, and the current environment reinforces this validity. Put another way, hyperscale cloud is doing exactly what it was meant to do.

The effect of rising energy costs on the hyperscale cloud vendors has been negative but comparably modest so far. Amazon cited a 200bps impact to AWS margins in aggregate over two years, and for Microsoft we expect an impact of less than 100bps to its cloud margins this financial year, unless costs rise significantly higher. The cloud vendors are absorbing these higher costs in the near term, but we believe they possess the pricing power to share rising costs with customers over the longer term. An underappreciated point is that the energy efficiency of hyperscale data centres is far superior to what customers can achieve on their own, which is further demonstrating to these customers the advantages of being in the cloud.

Cloud computing is proving its value to customers as much in this environment as it ever has, and we can see this when we delve beyond the quarterly headlines. It is why we continue to view this investment opportunity as compelling on the longer time horizon. It is an attractive, enduring, and multi-year opportunity that will deliver robust growth and attractive margins on the other side of the economic cycle we find ourselves in today.

By Adrian Lu, Investment Analyst

Sources: Company filings and Magellan estimates

Important Information:

This material is not intended to constitute advertising or advice of any kind and you should not construe the contents of this material as legal, tax, investment or other advice. In making an investment decision, you should read and consider any relevant offer documentation applicable to any investment product or service and must rely on your own examination of the same and consider obtaining professional investment advice tailored to your specific circumstances before making any investment decision.

The investment program of the strategy or strategies presented herein ('Strategy') is speculative and may involve a high degree of risk. The Strategy is not intended as a complete investment program and is suitable only for sophisticated investors who can bear the risk of loss. The Strategy may lack diversification, which can increase the risk of loss to investors. The Strategy's performance may be volatile. Past performance is not necessarily indicative of future results and no person guarantees the future performance of the Strategy, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs and such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. This material may contain ‘forward-looking statements’. Actual events or results or the actual performance of the Strategy or any financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. The Strategy will have limited liquidity, no secondary market for interests in the Strategy is expected to develop and there are restrictions on an investor's ability to withdraw and transfer interests in the Strategy. The management fees, incentive fees and allocation and other expenses of the Strategy will reduce trading profits, if any, or increase losses.

No representation or warranty is made with respect to the correctness, accuracy, reasonableness or completeness of any of the information contained in this material. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. This material may include data, research and other information from third party sources. No guarantee is made that such information is accurate, complete or timely and no warranty is given regarding results obtained from its use. The issuer of this material and its related entities and affiliates will not be responsible or liable for any losses, whether direct, indirect or consequential, including loss of profits, damages, costs, claims or expenses, relating to or arising from your use or reliance upon any part of the information contained in this material including trading losses, loss of opportunity or incidental or punitive damages.

This material and the information contained within it may not be reproduced, or disclosed, in whole or in part in any circumstances. , Further information regarding any benchmark referred to herein can be found at www.magellaninvestmentpartners.com/funds/benchmark-information/. Any third-party trademarks contained herein are the property of their respective owners and are used for information purposes and only to identify the company names or brands of their respective owners. (060126-#i1)

United Kingdom: This material has been prepared by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners and is distributed in the United Kingdom by Magellan Investment Partners (UK) Limited (FRN: 1037936), an appointed representative of Sentinel Regulatory Services Ltd (FRN: 1007093) which is authorised and regulated by the Financial Conduct Authority. This material does not constitute an offer or inducement to engage in an investment activity under the provisions of the Financial Services and Markets Act 2000 (FSMA). This material does not form part of any offer or invitation to purchase, sell or subscribe for, or any solicitation of any such offer to purchase, sell or subscribe for, any shares, units or other type of investment product or service. This material or any part of it, or the fact of its distribution, is for background purposes only. This material has not been approved by a person authorised under the FSMA and its distribution in the United Kingdom and is only being made to persons in circumstances that will not constitute a financial promotion for the purposes of section 21 of the FSMA as a result of an exemption contained in the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (FPO) as set out below. This material is exempt from the restrictions in the FSMA as it is to be strictly communicated only to 'investment professionals' as defined in Article 19(5) of the FPO.

United States: This material has been prepared by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners (‘Magellan’) which is a registered investment adviser. The investment strategies described herein are offered in the United States by Magellan Investment Partners North America, Inc., a U.S.-registered investment adviser. Magellan and Magellan Investment Partners North America, Inc. are affiliated entities for purposes of the Investment Advisers Act of 1940. Registration as an investment adviser does not imply any level of skill or training. This material is not intended as an offer or solicitation for the purchase or sale of any securities, financial instrument or product or to provide financial services. It is not the intention of Magellan to create legal relations on the basis of information provided herein. Past performance does not guarantee future results. Where performance figures are shown net of fees charged to clients, the performance has been reduced by the amount of the highest fee charged to any client employing that particular strategy during the period under consideration. Actual fees may vary depending on, among other things, the applicable fee schedule and portfolio size. Fees are available upon request and also may be found in Part 2 of Magellan’s Form ADV.

Canada: This material is provided to you by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners (‘Magellan’). Magellan is not registered in any province in Canada. The head office of Magellan is in Sydney, Australia and all or substantially all of its assets are situated outside of Canada. Due to the foregoing, there may be difficulty enforcing legal rights against Magellan.

South Africa: This material is provided to you by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners, who in accordance with FAIS Notice 55 of 2023 issued by the Financial Sector Conduct Authority, Magellan Investment Partners is exempted from section 7(1) of the Financial Advisory and Intermediary Services Act, 2002 (Act No. 37 of 2002). This material is not an offer in terms of Chapter 4 of the Companies Act, 2008.

UAE: This material has been produced by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners. This material is not for distribution to any other person. This material, and the information contained herein, does not constitute, and is not intended to constitute, a public offer of securities in the United Arab Emirates (‘UAE’) and accordingly should not be construed as such. Any offer of securities or financial services is made only to a limited number of exempt Professional Investors in the UAE who fall under one of the following categories: federal or local governments, government institutions and agencies, or companies wholly owned by any of them. No securities or services have been approved by or licensed or registered with the UAE Central Bank, the Securities and Commodities Authority, the Dubai Financial Services Authority, the Financial Services Regulatory Authority or any other relevant licensing authorities or governmental agencies in the UAE (the ‘Authorities’). The Authorities assume no liability for any investment that the named addressee makes as a Professional Investor. This material is for the use of the named addressee only and should not be given or shown to any other person (other than employees, agents or consultants in connection with the addressee’s consideration thereof).

Japan: This material is prepared by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners. The content is for informational purposes only and directed at Qualified Institutional Investors and other professional investors as defined in the Financial Instruments and Exchange Act. No distribution of this material will be made in any jurisdiction where such distribution is not authorised or is unlawful. This material does not constitute, and may not be used for the purpose of, an offer or solicitation in any jurisdiction or in any circumstances in which such an offer or solicitation is unlawful or not authorized or in which the person making such offer or solicitation is not qualified to do so.

Other jurisdictions: This material is provided to you by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners. No distribution of this material will be made in any jurisdiction where such distribution is not authorised or is unlawful. This material does not constitute, and may not be used for the purpose of, an offer or solicitation in any jurisdiction or in any circumstances in which such an offer or solicitation is unlawful or not authorized or in which the person making such offer or solicitation is not qualified to do so.